I booked my travel insurance with Direct line last year for the U.S . told them I was riding a 1200 gs .Policy arrived stating only covered for bikes up to 125 cc.

phoned Direct line who clearly stated I would not be covered for public liability or medical cover . I did mange to get a policy through J S Insurance which cost 60% more and turned out to be totally useless when i did need it.

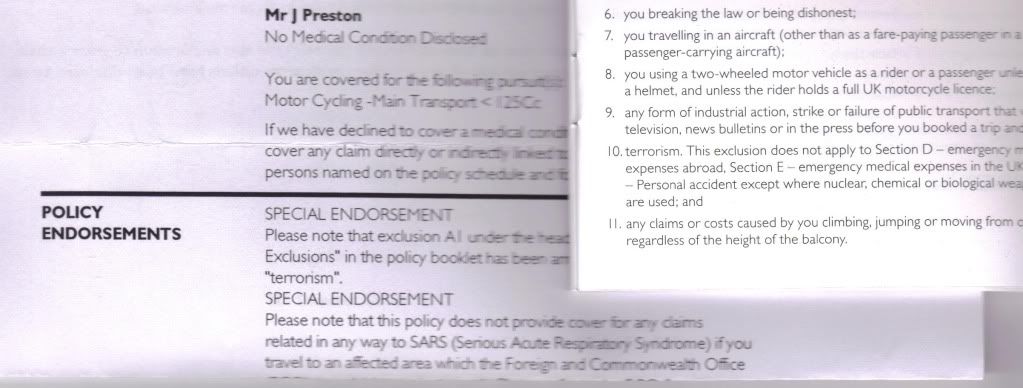

In post 65 above same issue:-

I also am insured with Direct Line, and previously was engaged in correspondence with them re motorcycle cover. Long story short, some call centre person told me I was not covered for over 125cc, eventually got letter confirming that I was covered on any m/c as long as full licence / helmet etc., No cost asked for.....

They need to get their story straight, I am still with them for Europe cover and understand that I am covered for the GS..